Bioprospecting Economy

Background

Biodiversity Economy at a glance

Many nations are legislating access to their biological and genetic resources for bioprospecting purposes. South Africa is one of these nations, with the country recently promulgating regulations to govern bioprospecting, access and benefit-sharing activities in accordance with its obligations as a signatory to the Convention on Biological Diversity.

South Africa is the third most biological diverse country in the world. Conservation of the countries natural genetic diversity is thus of strategic value to the provision of ecosystem services, now and in the future as these are the natural laboratories of the country. This biological richness also provides an important basis for economic growth and development.Use of these resources in bioprospecting offers the opportunity to create additional employment in the country, as shown by a number of notable industries that have developed within biological resources use sector of South Africa.

Export and use of South Africa's biodiversity, particularly indigenous plant resources and bee products, are however not well documented which may be limiting the benefits which we derive from them. The effective implementation of the legislative provisions on the use of indigenous biological resources and the effective support of small business development in this field are reliant on a sound knowledge and understanding of the bioprospecting market sectors.

One of the key benefits of the method applied in the sizing of the indigenous plant and bee product bioprosecting market is the collection of new, primary data on the industry. Primary data was collected through two methods: store sampling and industry interviews.

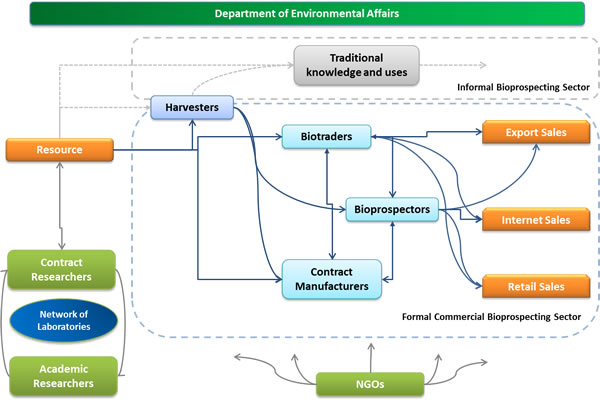

A bioprospecting commercial industry value chain was developed showing the key role players, from the resource to the end user. This value chain was used to describe the indigenous plant resources and bee products currently utilised in the formal commercial bioprospecting sector of South Africa. Although there is also an informal bioprospecting sector value chain which demonstrates much overlap with the formal commercial bioprospecting sector, this informal market for indigenous resource-based products was not included in this market sizing. The report thus provides a picture of one aspect of a much larger bioprospecting trade market.

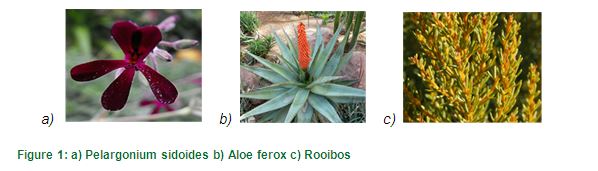

In a survey of retail and specialist stores and health shops across the country, 549 retail products were found to contain South African indigenous plant resources and bee products. The resources included in these products where however, limited to only 24 South African plant species. The largest resource use in products was Aloe ferox, followed by bee products, rooibos and Pelargonium sidoides as illustrated below:

Based on South Africa’s Bioprospecting, Access and Benefit-Sharing Regulatory Framework, Guidelines for Providers, Users and Regulators, the bioprospecting industry can be segmented into 10 product categories. These segments include medicines, industrial enzymes, essential oils, food flavourants, fragrances, cosmetics, emulsifiers, oleoresins, colours, extracts and new plant varieties (DEA, 2012). The internet search and survey of stores in South Africa indicated that bioprospecting products could only be found in 5 of these bioprospecting market segments; namely cosmetics, oils, food falvourant, frange and medicine (complementary medicine). No products containing indigenous biological resource were thus found in the emulsifier, oleoresins, extracts and colours market segments. New plants were not included in the market sizing.

The size of the bioprocessing segment of the value chain, as measured by total revenue generated in the bioprocessing segment (primary and secondary processing of indigenous resources) of the bioprospecting market, was approximately R482 million in 2011. Of this, approximately R322 million was exported. The remainder, R160 million, was transformed into value-added products sold within the domestic retail sales market.

The total revenue produced from value-added products sold in the domestic retail market, and which contained bio-resources as an ingredient, was approximately R1,470 million in 2011 (DEA Bio-products retail database). These locally produced value-added products can be segmented into five product categories:

- Personal hygiene products (R585 million or 40% of products)

- Cosmetics (R555 million or 38% of products)

- Complementary medicines (R170 million or 11% of products)

- Food flavourings (R110 million or 8% of products)

- Oils (R50 million or 3% of products).

The importance of indigenous plant resources and bee products as an ingredient in these value-added product categories is revealed by the comparative values of retail sales of products with and without these indigenous resources as an ingredient. Products containing indigenous plant resources and bee products as an ingredient sell between 50%-100% more by retail value than products without indigenous plant resources and bee products as an ingredient (DEA Bio-products retail database). This is evident of a strong consumer demand for products containing indigenous plant resources and bee products as an ingredient.

The potential market size of the bioprospecting industry, based on resource permit application data, is at least R2, 150 million per year. This means that the current industry has reached only about 20% of its potential, and thus has a large growth potential. This market may grow to between R600 and R800 million over the next 5 years (2018).

The bio-resources economic sector is, for many reasons, an ideal development sector in the South African context. There are several reasons for this:

- It realises the economic value of indigenous species;

- It facilitates rural economic development;

- It has very high value added potential;

- It has a high potential to earn foreign currency;

- It enables the development of new product markets;

- It is a 100% renewable industry.

Based on this data, the GDP contribution of cultivation, wild harvesting and bio-trading in 2011 was approximately R82 million in 2011. Thus, although this is currently a relatively small industry, the growth potential of the industry is large, and there remains much potential for GDP growth. This GDP contribution will grow with market growth and may be expected to increase to between R115 million to R150 million per year by 2018. This will be highly beneficial to rural economic development.

The sector currently earns foreign currency through exports of indigenous plant resources. The total value of these exports was approximately R322 million in 2011. The medium term outlook for Rand to US$ exchange rates is 9.5 R/US$ (Rand Merchant Bank). This medium term weakening of the Rand is positive for this sector as it would increase export revenues.

The bioprospecting sector is an important job creation sector. Job creation occurs throughout the whole value chain. It is possible that an additional 700 to 1,700 new jobs may be created in this industry, by 2018, depending on the market growth trajectory achieved.

Following the bioprospecting value chain segmentation, three key segments require strategic intervention to remove industry supply constraints and achieve conservation goals. These segments are the (1) Wild harvesting segment; (2) Cultivation segment and (3) Bioprocessing segment.

The bioprospecting industry has a large growth potential. There is a large potential for local value adding in the contract manufacturing and bioprospecting sectors. The multiplier effect of cultivation and harvesting of indigenous plant resources is approaching 10.00. This is therefore a highly effective value adding sector, and investment in this sector will be accompanied by a large multiplier effect.

South Africa Bioprospecting Value Chain

A bioprospecting commercial industry value chain was developed by the project team through engagement with stakeholders in a workshop in Pretoria and Cape Town. The value chain shows the key role players in the commercial sector, from the resource to the end user. This value chain is used to describe the indigenous plant resources and bee products currently utilised in the formal commercial bioprospecting sector of South Africa, discussed in the sections below.

It should be noted that there is also an informal bioprospecting sector value chain which demonstrates much overlap with the formal commercial bioprospecting sector in Figure 2. The informal market for indigenous resource-based products is estimated to be extremely large and can be found in all provinces of the country. A number of research studies have been conducted on the informal trade of biological resources in South Africa. According to a study of the Economics of the Traditional Medicine Trade in South Africa by Mander et al. (undated):

- The traditional medicines market in South Africa is estimated to be worth R2.9 billion per year; representing 5.6% of the National Health Budget;

- There are 27 million consumers of traditional medicines;

- At least 133 thousand people are employed in the trade in traditional medicines;

- The traditional medicine market is supplied by 771 plant species.

The focus of this market sizing is however, the formal commercial bioprospecting market, specifically products containing indigenous plant resources and bee products in South Africa. This market sizing focussed on collecting data and information of bioprospecting products which are traded in the local or international commercial market. This market sizing thus provides a picture of one aspect of a much larger bioprospecting trade market.

Figure 2: Bioprospecting value chain in South Africa showing the informal and formal commercial bioprospecting sectors which make up the overall bioprospecting value chain of the country. The informal bioprospecting sector value chain is not included in the market analysis

Based on the definition of bioprospecting, namely the processing of indigenous biological resources from ‘raw material’ up to the point where the resulting product is ready to be sold to consumers, the above value chain documents the role players in the sector up until the product can be sold to the consumer.

Since it is not always clear which role player in the value chain is required to apply for a bioprospecting permit, DEA has adopted the approach that any person dealing in biodiversity with the intention to trade is required to apply for a bioprospecting permit.

According to DEA (2012), cultivation of indigenous biological plant resources or the trade in raw material in its original form, for example rooibos plants, may be bioprospecting, depending on the use of the resource. That is, if rooibos tea is cultivated for the beverage market and sold as a tea, it is not bioprospecting but if the plant is used to make an extract for incorporation into another product this is considered bioprospecting. Whether or not traders must apply for a bioprospecting permit will depend on the ultimate goal of their actions.

The roles of the various stakeholders in the value chain in Figure 2 are discussed in more detail below.

The value chain initiates at the indigenous biological resource.NEM: BA (South Africa, 2004) defines an indigenous biological plant resource (hereafter referred to as a resource) as a resource that includes any living or dead animal, plant or other organism of an indigenous species, their derivatives and genetic material, gathered from the wild or accessed from any other source, including cultivated, bred or kept in captivity or cultivated or altered in any way by means of biotechnology (South Africa, 2004). These resources are owned or controlled by the owner of the land on which the resource occurs (DEA, 2012). This may be an individual farmer, a community, a government agency or a parastatal (DEA, 2012).

Researchers in the value chain are usually involved in the discovery phase of bioprospecting where the resource is being explored for potential uses (DEA, 2012). The Act and the BABS Regulations make a distinction between the ‘discovery phase’ of bioprospecting initiatives and the ‘commercialisation phase’. In the discovery phase, researchers attempt to find out if an indigenous biological resource has any potential to be further developed into a commercial product. In the commercialisation phase, commercial potential has already been identified in the indigenous biological resource (South Africa, 2004; DEA, 2012). Researchers very often work with Traditional Knowledge Holders, who are the individuals or communities which have the knowledge of how the resource is utilised. Researchers are usually focused on a particular sub-sector of resource application within the bioprospecting value chain. For example research may focus on:

- Discovering resources which may play a role in the bioprospecting market i.e. research into the application of the resource or on the active components of the indigenous plant resource which is of value to the market;

- Discovering the use of resources within a specific sector in the market. For example the use of the resource in the pharmaceutical market (i.e. conventional medicines); research into resource use in the herbal and nutraceutical market;

- Discovering the sustainable resource utilisation by focusing on cultivation of the resource and agricultural processes related to this to ensure the quality of bioprospecting products (i.e. research conducted by the Department of Agriculture, Forestry and Fisheries and the Agricultural Research Council).

- Sharing knowledge of bioprospecting or resource use in the country - knowledge brokers (e.g. the book by van Wyk et al, 2009 on Medicinal Plants of South Africa is knowledge brokering)

Harvesters in the value chain are those individuals which provide the indigenous species product. This may include harvesting of the resource from the wild or from cultivated small (<1 ha) to larger (>5ha) farms. An indigenous species according to NEM: BA (2004) is any species that occurs, or has historically occurred, in a free state in nature within the borders of South Africa. It excludes any species that has been introduced to South Africa as a result of human activity (South Africa, 2004). Species utilised in the bioprospecting market of South Africa are sourced in three ways; namely:

- Wild harvesting where the resource is collected in the wild (i.e. natural habitat of the species), usually by poor rural harvesters.

- Cultivation where the species is domesticated and cultivated (farmed). South Africa has already gone some way to cultivation of indigenous species on small-scale (quarter to 1 ha) rural farms, usually by disadvantaged individuals. Some larger scale (>5 ha) commercial cultivation of species has also occurred, relating particularly to rooibos and buchu.

- The third category, synthetic production where the required natural resource ingredient is synthetically, is not included in this market sizing.

Biotraders are the persons who are engaged in biotrading activities (DEA, 2012). Biotrading is a form of/type of bioprospecting. Biotrading according to the South Africa’s Bioprospecting, Access and Benefit-Sharing Regulatory Framework includes any activity relating to the commercial collection, processing and sale of products derived from biodiversity. When described as Biotrade it is often linked to criteria of environmental, social and economic sustainability (DEA, 2012). Biotraders and biotrading in South Africa is regulated through a permit system under the above mentioned regulations. In this study we class any individual or organisation trading in the raw materials or organisation trading in the primary processed indigenous plant resource as a biotrader i.e. buys and sells the fresh or dried components of a plant or the dried and sliced, milled or powdered components of the plant.

Contract manufacturer in this value chain are the individuals or organisations involved in the developing of intermediate products for the bioprospecting market. Contract manufacturers are those individuals or organisations which are contracted to produce a specific intermediate for the bioprospector (i.e. primary processed raw resources). In this study we class any individual or organisation trading in the semi-process (primary processed) form of the indigenous plant resource such as the oils, extract or tinctures as a contract manufacturer.

Bioprospector (secondary manufacturer and/or marketer) in the value chain are the individuals or organisations which manufacture and handle the secondary processed or final product i.e. process the materials bought from the biotrader or contract manufacturer into the final product or an individual or organisation who sells these final products. The bioprospector is thus the final product producer/manufacturer of the bioprospecting value chain.

Exports, according to NEM:BA, are those products which are taken out or transferred from a place within the Republic of South Africa to another country or to international waters (South Africa, 2004). Export buyers include a group of individuals and organisations which trade in the raw or value-added products for onward sales to industries and processors. South Africa has a high volume of resource-based products exported in the raw form. This market is however dominated by only a few species such as raw Aloe ferox (bitter aloe) and Harpagophytum procumbens (Devils claw) which are used internationally in pharmaceutical products. The South African export market of the indigenous plant resources has the potential for diversification of species such as Hoodia gordonii and Adansonia digitata (Baobab) which are used in international nutraceutical market and export of Sclerocarya birrea (marula) and Citrullus lanatus (Kalahari melon) for the international cosmeceutical market. However, this will result in the value-add to the use of South African indigenous plant resource being very limited.

Retail Sales and Internet Sales in the value chain, includes products marketed and sold through health shops, pharmacies, internet-based marketing and ordering, formal mail-order systems, wholesales and middle-men and directly from manufacturers. In this market sizing we separate this group of traders into:

- Internet trade:bioprospecting products sold through the internet; and

- Retails trade: bioprospecting products sold through:

- Retails stores such as Spar, Checkers, Pick n Pay;

- Specialist stores such as Dischem and Clicks; and

- Health stores which focus on selling health products.

Non-governmental Organisations are those organisations involved in the bioprospecting market which are not linked to government. NGOs have various roles to play in the bioprospecting value chain, including:

- Trade association involved in the trade or marketing of specific resource i.e. Phyto Trade

Sub-sector associations which represent a specific group of members within the bioprospecting value chain i.e. National Health Products Association of South Africa; South African Essential Oils Producers Associations and South African Honeybush Association.

Segmenting of the formal bioprospecting market in South Africa

Internationally the natural plant and organic sector is considered to be the fastest growing sector of the agribusiness industry. Growth in sales of nutritional products in the US alone increased from US$ 15 billion in 1999 to US$ 23 in 2002 (Kelly et al., 2005). Approximately 85,000 plant species are reported to be used for medicinal purposes, with the US leading the market share (35%). Africa only contributes less than 1% of this market (US$ 520) (de Kock, 2004 in Makunga et al., 2008).

The bioprospecting market in South Africa has a number of categories of biological products produced using indigenous resource-based components. These biological products can be categorised as (Mander and le Brenton, 2005):

- Crude/raw biological products which include unprocessed biological products such as saps, gels, leaves, bark. Mander and McKenzie (2005) estimate that 5,000-10,000 tonnes of raw materials are being traded in the formal bioprospecting market of South Africa. These raw materials are collected from the wild by rural harvesters and are commercially farmed.

- Herbal products which are processed biological-based products that have therapeutic qualities which are not formally, legally recognised i.e. these products are found at traditional markets and are recognised in this informal market for the therapeutic qualities;

- Allopathic products which are biological-based medicinal or pharmaceutical products with formal legally recognised therapeutic qualities. These products are often referred to as phytomedicines. These products are usually based on a single species product that has been stabilised using conventional pharmaceutical technology and have a proven track record of medical efficiency. Phytomedicines products usually take the form of a tincture, tablet, capsule or mixture.

- Therapeutic products which are nutraceutical and cosmecuetical products containing some indigenous biological ingredient.

- Nutracueticals are food products containing indigenous resources which are consumed for their therapeutic benefits. The nutraceutical market in South Africa is relatively small but is however, growing. These products include beverages (herbal teas and fruit juices), cereals and nutritional supplements containing indigenous biological resources. The domestic nutraceutical market in South Africa had an estimated value of R7bn in 2004. South African Ready-to-Drink (RTD) market grew by 14% in total value in 2008 and is estimated to be worth R 442million (Keiser Association, 2010).

- Cosmeceuticals are cosmetic and personnel care products which contain indigenous resources. Products of this nature have been increasing and include hair care, skin care and bath products. The South African market for cosmetics was estimated to be worth R24bn in 2007, with expected growth of 15-20% per year. Natural ingredients are also increasingly popular in South African cosmetic products (Keiser Association, 2010).

Based on these categories, this assignment categorizes the products with South African indigenous plant resources and bee products in them into the categories shown in Table 1.

| Category | Definition |

|---|---|

| Natural dyes and colours |

Dyes and colours prepared using indigenous plant resources |

| Cosmetic |

A preparation, such as powder or a skin cream, designed to beautify the body by direct application. In this market sizing all facial and body creams, balms and products were categorised as cosmetic |

| Personal hygiene products |

A sub-category of the cosmetic products. Includes products other than facial or body creams, balms of products such as shampoo, conditions, sunscreens, soap, deodorants |

| Emulsifier |

Any agent that forms or preserves an emulsion, esp. any food additive, such as lecithin, that prevents separation of sauces or other processed foods |

|

Oil |

A liquid that is generally distilled (most frequently by steam or water) from the leaves, stems, flowers, bark, roots, seeds, fruits or other organs of a plant |

|

Extract |

A preparation containing the active principle or concentrated essence of a material |

|

Food flavourant |

An indigenous plant resource which is added to food as a flavour |

|

Fragrance |

Generally essential oils which are used in the fragrance industry |

|

Medicine |

any drug or remedy for use in treating, preventing, or alleviating the symptoms of disease |

|

Allopathic medicines |

Are subject to registration in terms of The Medicines and Related Substances Act; Act 101 of 1965, as amended. |

| Complementary medicines |

Includes Anthroposophical medicines, Aromatherapeutic medicines, ayurvedic medicines, Chinese medicines, energy substances, homeopathic medicines, nutritional substances with therapeutic effects, Western herbal medicines, Unani Tibb medicines, combination homeopathic / Flower essence, and combination complementary medicines. |

| African Traditional Medicines |

Herbal products traded on the informal market. These products are not included in the market sizing. |

|

Oleoresin |

Any semisolid mixture of a resin and essential oil, obtained from certain plants |

Related documents

Resource Assessment for Aloe Ferox in South Africa

The Report on the study (Resource Assessment for Aloe ferox in South Africa) indicates that the plant is distributed throughout the Western Cape, Eastern Cape, Free State and KwaZulu-Natal Provinces and is one of the most frequently used indigenous biological resource in the bioprospecting industry in the country. It further possesses economic benefits for communities where they occur and is likewise utilised commercially in the pharmaceutical and cosmetic industries.

National Biodiversity Economy Strategy (NBES)

The biodiversity economy of South Africa encompasses the businesses and economic activities that either directly depend on biodiversity for their core business or that contribute to conservation of biodiversity through their activities. The commercial wildlife and the bioprospecting industries of South Africa provide cornerstones for the biodiversity economy and are the focus of this strategy.

EcoInvest III: Biodiversity economy strategy

This Strategy is positioned at a time when the international community is approaching the review of the Aichi Targets, and the drive towards knowledge, understanding and implementation of “green economies” is prompting a paradigm shift away from business as usual. These elements underline the importance of inclusive dialogue and knowledge sharing with key stakeholders around the role and potential for developing a biodiversity economy in the Province.

Related links

- Aloe Council: http://www.aloesa.co.za/

- Rooibos Council: https://sarooibos.co.za/

- SABS: https://www.sabs.co.za/standardss/standards_about.asp http://www.aloesa.co.za/

- Cape Bush Doctors:http://www.cbd.org.za/

- Traditional Leaders Association: http://search.info4africa.org.za/Organisation?Id=91141

- The Cosmetic, Toiletry & Fragrance Association:http://www.ctfa.co.za/

References

- DEA (2012). South Africa’s Bioprospecting, Access and Benefit-Sharing Regulatory Framework. Guidelines for Providers, Users and Regulators. DEA, Pretoria.

- Kaiser Associates Economic Development Practice (2010). Rooibos and Honeybush market development programme framework. Revised final report.Western Cape Department of Economic Development and Tourism.

- Kelly, J.P., Kaufman, D.W., Kelley, K., Rosenberg, L., Anderson, T.E. and Mitchell, A. (2005). Recent trends in use of herbal and other natural products. Archives of Internal Medicine 165: 281–286.

- Mander, M. and Le Breton, G. (2006). Overview of the medicinal plant industry in Southern Africa. In: Diederichs, N. (Ed.). Commercialising Medicinal Plants: A Southern African Guide. Sun Press, Stellenbosch, pp. 43–52.

- Mander, M. and McKenzie, M. (2005). Southern African trade directory of indigenous natural products. http://www.cpwild.co.za/DocTrade.htm.

- Mander, M., Ntuli, L., Diederichs, N. and Mavundla, K. (undated). Economics of the Traditional Medicine Trade in South Africa. [Online]. Available: http://www.hst.org.za/uploads/files/chap13_07.pdf.

- South Africa (2004) National Environmental Management Biodiversity Act, No 10 of 2004. Government Printers, Pretoria, South Africa.